Synthesis of the systematic literature review

Financial inclusion and the digital divide among older adults

Technological factors such as facilitating conditions, performance expectancy and effort expectancy have consistently emerged as key enablers of intention and use (Venkatesh et al., 2012). Despite the immense potential of communication technologies and advanced internet services, older adults continue to be marginalized in the digital financial ecosystem (Ge et al., 2025). FinTech presents a promising solution to bridge this gap by delivering cutting-edge, user-friendly, and accessible FinTech solutions (Roh et al., 2024, Noreen et al., 2022). However, even with the rising ownership of technology among this demographic, their engagement with the digital financial services remains limited (Choi et al., 2024). This suggests that beyond access, psychological, cognitive, and social enablers must be considered to understand actual usage (Zaid et al., 2023). To better understand this limited participation, it is crucial to examine the specific underlying drivers and barriers that influence FinTech adoption among older adults (Tomczyk et al., 2023).

Operational definitions

‘Older adults’ are defined as individuals aged 60 years or older, in accordance with the UNHCR emergency handbook (UNHCR, 2025). However, we acknowledge that this demographic is not homogenous (Tomczyk et al., 2023). ‘FinTech’ as an umbrella term, refers to technology- driven financial services and platforms designed to enhance user experience by offering more user-friendly, transparent, efficient, and automated solutions for managing, accessing or transacting financial products (Dorfleitner et al., 2017).

Key drivers of FinTech adoption among the older population

Extant literature has explored the factors that affect FinTech adoption among older population. For instance, according to Arenas-Gaitán et al. (2015), the acceptance of internet banking among older adults is strongly influenced by performance expectancy, effort expectancy and price value. Their study concluded that older people’s actual behaviour is shaped by both behavioural intentions and habits. In this context, Graf-Vlachy and Buhtz, (2017) found that older adults’ FinTech adoption is significantly determined by the amount of time they spend using digital technologies, their digital experience and exposure. This aligns with the personal-cognitive domain, especially digital literacy and self-efficacy (Czaja et al., 2006; Jena & Paltasingh, 2025). Similarly, another study highlights that older adult’s positive attitudes toward mobile payment enhances their intention to use these technologies. This study found that perceived usefulness (PU), perceived ease of use (PEOU) and observability positively shape attitudes towards mobile payments (Yang et al., 2023).

Furthermore, Lee and Coughlin, (2015) identified ten core determinants for older adults’ adoption of technology. These includes usability, value, accessibility, affordability, social support, technical support, independence, emotion, confidence and experience. Many of these map directly to constructs such as hedonic motivation, trust, and attitude, categorized in the social and psychological factors of the conceptual model (Li & Kostka, 2024; Weck & Afanassieva, 2023). Adding to this, a study conducted in the United States by Wang and Pradhan, (2020) revealed that trust plays a significant role in influencing older adults’ willingness to use robo-advisors for their personal finances. Notably, trust operates both as a driver and, when absent, a barrier—this duality is acknowledged in our conceptual framework (Mei, 2024). While these factors explain adoption motivators, several barriers still hinder the actual usage of digital financial services among the older population.

Barriers to the adoption of digital financial technology among older adults

It is often claimed that human considerations are not adequately incorporated into product design and services. Even though older adults frequently lack awareness or knowledge of existing ICTs and related assistive technologies (Heinz et al., 2013, Kramer, 2014) there remains limited focus on innovative solutions to overcome barriers for this population (Wang & Pradhan, 2020). Moreover, older adults are typically conservative, cautious, sceptical, and risk-averse in adopting innovations, often preferring to observe their success among peers before engaging. Additional barriers identified within this cohort include cognitive, physical, attitudinal and socio-economic challenges (Wu et al., 2015). Key psychological and emotional barriers such as anxiety, security concerns, and perceived risk are consistently cited in the literature (Dizon & Ebardo, 2025).

This systematic review on barriers and enablers bring technological enablers alongside personal-cognitive factors in ensuring effective adoption of FinTech among older adults. However, the infrastructural differences and individual-level heterogeneity varies across countries, that may lead to diverse adoption and impact of digital finance among older adults. These findings necessitate development of a descriptive understanding of emerging trends of research manuscripts. The following section based on the bibliometric analysis demonstrate a temporal, geographical and academic source-based pattern of the research manuscripts.

Bibliometric analysis of scientific output and publication sources

Trend in annual scientific production of manuscripts

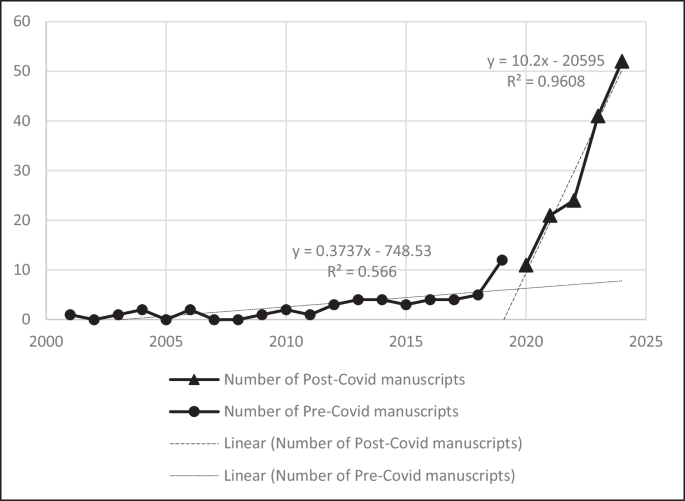

Figure 4 represents the trend in annual scientific production, showing the number of articles published each year. Prior to 2012, research on financial inclusion was limited (Allen et al., 2012), with foundational studies focusing more on access to health services rather than financial technology for older adults (Heart & Kalderon, 2013). Scholarly attention to senior citizen’s financial inclusion was hindered by digital gap (Yang et al., 2025). Research expanded during the second decade of twenty-first century, driven by the G-20 summit in Pittsburgh held in the year of 2009, highlighted universal financial access by 2020 with specific focus on policy-oriented studies. Although early studies did not emphasise older adults, they gradually began to highlight the distinct financial and technological challenges faced by this demographic. The growth between 2010-2019, was driven by factors such as rapid digitalization, mobile banking, and targeted financial literacy efforts for older adults. Research on FinTech adoption among older adults has increased, with 141 publications examining post-pandemic digital transformation and the usability of older population friendly banking between 2021 and 2025. Although financial inclusion policies after 2006 laid the groundwork for the research, older adults received limited attention until 2015 (Arun & Kamath, 2015). Since 2016, there has been a rising recognition of older peoples’ digital challenges and their limited FinTech footprints (Jena & Paltasingh, 2025). COVID-19 became a turning point (Sixsmith et al., 2022), shifting focus to digital banking access as a key priority (Vilhena & Navas, 2023). Research from 2021 to 2025 reflects a growing interdisciplinary focus on financial literacy, FinTech usability, and digital security challenges for older adults (Gumilar et al., 2024).

Trend analysis of annual scientific production of manuscripts, Source: Author’s own elaboration using bibliometrix R package.

To quantify these patterns, a bi-variate linear regression model representing the changes in number of publications (y) over the years (x) is stated in equation-1.

$$\,\begin{array}{cc}{\rm{y}}=1.3983{\rm{x}}-2805.8, & {{\rm{R}}}^{2}=0.5409\end{array}$$

(1)

In this case, the time variable accounts for about 54% of the observed variation, and the positive slope of the regression line (1.3983 with p < 0.05) highlights a long-term growth trajectory in annual publications, However, the moderate R2 value also indicates that a simple linear model does not fully capture the recent acceleration in scholarly output. To provide a clearer understanding on this regard, Fig. 4 demonstrates the change in the slope of the number of publications pre-COVID period (b = 0.374, R2 = 0.566) and post-COVID period (b = 10.2, R2 = 0.96). An interrupted time-series (ITS) analysis demonstrates that the gradient change (9.826 with Standard Error=0.725) in publications before and after 2020 has been statistically significant at p < 0.05.

Country-wise analysis of publication volume and citation impact

The country-wise analysis of publication volume and citation impact are presented in Table 2. The first panel presents the results obtained by VOSviewer from the analysis of 204 Scopus manuscripts, while the second panel shows the country-wise presentation based on the analysis of top 55 cited manuscripts obtained from Scopus database. The United States and China lead the list of the countries as the most productive ones, followed by United Kingdom and Australia. India, being the largest democracy and showing a rapid increase in older population, it is important to note the rise of studies in India, which can develop understanding for the emerging economies across the globe.

Most relevant sources

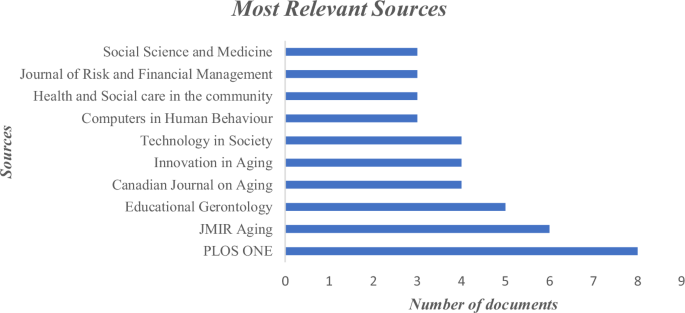

Figure 5 displays the top ten journals based on citations counts. The threshold was set at a minimum of one document and 100 citations per source. PLOS ONE emerges as the most significant source, with 8 documents, highlighting its prominence in contributing to the research domain. JMIR Aging stands out as the second-most relevant source, with 6 documents, followed by Educational Gerontology with 5 published documents, reflecting its relevance to studies on ageing and technology. Other significant contributors include Canadian Journal on Aging, Innovation in Aging, and Technology in Society, each contributing 4 documents.

Author’s own elaboration. Source: Data retrieved and analysed using the Bibliometrix R package (Biblioshiny).

Tree map of 50 prominent themes with paper counts and percentage

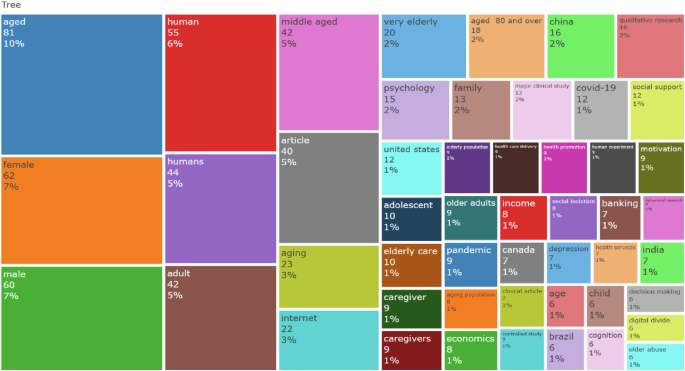

Figure 6 visualizes 50 prominent research themes displaying the number of manuscripts and relative percentage. A tree map was employed to analyse the primary topics based on the number of papers published. The topics discussed the most were aged (n = 81 manuscripts, 10%), followed by female (n = 62 manuscripts, 7%), male (n = 60 manuscripts, 7%), Human (n = 55 manuscripts, 6%), Humans (n = 44 manuscripts, 5%), adult (n = 42 manuscripts, 5%), middle-aged (n = 42 manuscripts, 5%).

Rationale for using both Bibliometric thematic mapping and keyword cluster analysis

We utilized bibliometric thematic mapping and keyword clustering with VOSviewer as part of the triangulation process to enhance rigour, validity, and richness to our bibliometric analysis through methodological triangulation. VOSviewer makes use of network visualization and clustering based on modularity to expose the structural relationships qualitatively, existing between research topics as addressed within extent literature. At the same time, Bibliometrix presents a broad depiction of the keywords, mapping themes based on the scale of centrality and density; thus classifying the constructs into core, niche, emerging, or underdeveloped areas (Arruda et al.; 2022).

Keyword thematic map

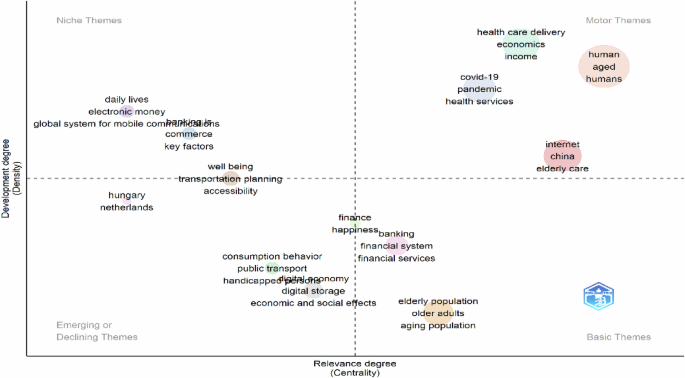

In this section, detailed analysis was made on the topics that researchers have given significance to, or they have focused their research in recent years. The primary research themes and topics within a given field can be found using the keyword thematic map. It makes it possible to quickly review the most popular study topics and the way keywords are distributed among various thematic clusters. Figure 7 presents a thematic map that categorizes key themes based on their relevance and development within the research field. The keywords in this visualization ‘daily lives, electronic money, global system for mobile communications, mobile payment, banking, commerce, key factors, mobile banking, well-being, transportation planning, accessibility, aging societies’ are niche themes with low centrality and high density, indicating they are well- researched but hold limited significance in the study area. Whereas, the keywords namely, ‘behavioural research, decision making, economic development, elderly population, older adults, aging populations, information and communication technology, technology adoption’ represent a fundamental theme with low density and high centrality and are considered as important but remains underdeveloped within the research field. The group of keywords including ‘banking, financial systems, financial services’ evolved from emerging/declining themes to basic themes. The upper-right quadrant represents motor themes characterized by high density and centrality indicating that they are both well- researched and important. The keywords belong to this quadrant are ‘human, aged, humans, health care delivery, economics, income, COVID-19, pandemic, and health services’. Themes appearing in the lower- left quadrant are either emerging or declining with low centrality and density and are regarded as under-developed with limited significance. The set of keywords enveloping ‘banking, financial systems and financial services’ evolved from emerging/declining themes to basic themes.

Thematic map illustrating conceptual structure of FinTech adoption among older adults.

Sensitivity analyses of bibliometric parameters

A minimum of five keyword occurrences was set as a threshold for thematic cluster analysis. In order to identify relevant sources, we set an eligibility criterion of at least one document and 100 citations per source. The network construction employed the association strength normalization technique, which is commonly used in bibliometric mapping to make items comparable. To test the stability of our results, we also varied the keyword thresholds (minimum = 3, 5 and 7 occurrences). The major keywords obtained from the five occurrences threshold criterion, such as ‘humans’, ‘aged’, ‘very elderly’, ‘aged 80 and over’, ‘older adults’, ‘ageing’, were consistently reproduced when we applied a lower (3) and a higher (7) occurrence thresholds. For three occurrences, 178 met the threshold out of 1546 keywords, and for seven, 45 keywords met the threshold. We similarly tested different source relevance thresholds considering 80, 100, and 120 citations, and alternative ways of normalizing the other metrics. The thematic clusters, leading sources, and country contributions remained largely the same across the two variations. These sensitivity analyses thus confirm the robustness of our bibliometric results.

Thematic cluster analysis

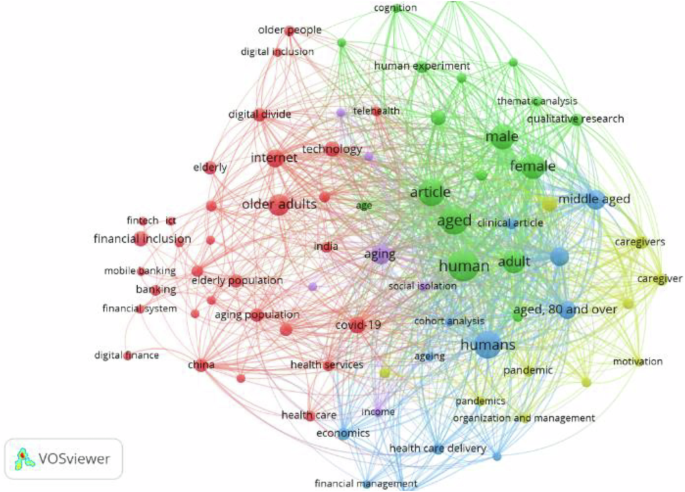

Despite the fact that Bibliometrix offers thirteen thematic cluster, and VOSviewer depicts five clusters, the in-depth thematic cluster analysis is done based on five clusters only. The patterns of networks connecting the keywords provide a better logical understanding on the dynamics of ongoing research. A minimum threshold of five keyword occurrences was applied. Figure 8 displays the keyword co-occurrence network, highlighting dominant research theme. The cluster analysis, presented in Table 3, demonstrating five distinct research clusters. The analysis has been conducted using VOSviewer with robust empirical referencing, and maps evolving intersections of digital financial inclusion, cognitive engagement, healthcare financing, caregiving psychology, and social well-being among older adults. Each cluster highlights a distinct yet interconnected area, illustrating the multidimensional nature of aging in an increasingly digital and socio-economically evolving environment.

Keyword co-occurrence network showing dominant research themes.

Cluster 1: digital financial inclusion and ICT adoption

Cluster 1, represented by the colour red, captures the intricate relationship between digital financial inclusion, aging populations, and ICT adoption, with a strong geographical focus on India and China. Central keywords such as ‘Digital Inclusion, Older Adults, Financial Inclusion, ICT, and Mobile Banking’ indicate that research in this area primarily explores accessibility challenges, behavioural adoption patterns, and financial decision-making processes among older populations.

Recent empirical work by Jin and Fan (2022) underscores the significance of understanding older adults banking experiences in China to enhance accessibility of new digital banking platforms. In a complementary context, a study conducted in Taiwan found that attitude and behavioural intentions significantly influence mobile payment adoption among the older adults (Yang et al. 2023). Arenas-Gaitán et al. (2015) emphasized that enhancing older adult’s financial decision making necessitates improvements in web design, highlighting usability and aesthetic appeal as key facilitators of informed, confident choices in digital environments.

The results also reveal the presence of digital divide and variations in perception, where factors such as trust, financial literacy, and usability are particularly crucial for the uptake of FinTech products. Prior research highlights that the digital divide among older adults in China stems from low basic digital literacy, limited socio-economic resources, personal constraints, and privacy concerns. However, self-learning, intergenerational support and targeted digital training are found to be significantly improving older adults comfort levels with digital technologies (Xu, 2023).

Furthermore, the presence of Decision-Making and Behavioural Research keywords within this cluster highlights the significance of habit formation, risk perception and social influence in shaping older generations’ digital financial behaviours. Mei (2024) observes that older adults’ engagement with mobile banking platforms is notably shaped by peer interactions and word of mouth communication, which collectively influence their perceptions and willingness to adopt such technologies. Additionally, Arenas-Gaitán et al. (2015) demonstrates that behaviour intention and habit had an impact on the actual internet banking usage pattern. Trust emerges as a critical determinant of mobile payment utility and usability, exerting a substantial influence on behavioural intention to adopt such technologies (Yang et al. 2023). However, as Yang et al. (2023) further note, trust in the functionality and benefits of mobile payments tends to decline with heightened perceived risk. Moreover, the presence of keywords such as COVID-19, Health Services, and Sustainability within this cluster reflects increasing scholarly interest in how the pandemic accelerated mobile payment and digital banking adoption – especially for healthcare-related transactions. Empirical evidence suggests that older adults received increased support and encouragement to use digital payment methods in the context of the COVID-19 pandemic (Zhu et al. 2024). Notably, several studies within this cluster points to practical interventions such as structured digital literacy programmes, intergenerational interaction and individualized training as effective means to bridge the digital divide and empower older adults (Lee & Kim, 2019; Putrie, 2025).

Cluster 2: cognitive perspectives on internet use

As indicated in the VOSviewer analysis (green cluster), this thematic group emphasizes the cognitive, psychological, and social aspects of internet use among adults and older populations. A study conducted among Chinese adults found a strong positive correlation between internet use and cognitive function, suggesting that digital engagement can serve as a protective factor against cognitive decline (Jiao et al., 2025). Prominent keywords such as Cognition, Internet Use, and Social Support highlight the scholarly focus on the interplay between cognitive function, social relationships, and digital participation. A study by Wu et al. (2019) demonstrates that regular digital device usage is positively correlated with cognitive abilities. Older adults who did not use digital device daily exhibited lower cognitive skills compared to daily users. Similarly, Wang and Chen (2024) highlight that internet use among older adults significantly enhances social involvement, promoting both physical and mental well-being through stronger social networks.

Based on the research questions, researchers have employed diverse methods to understand the behavioural patterns and underlying factors associated with digital engagement in older age. The frequent appearance of terms such as Interviews, Qualitative Research, and Article, indicates a strong reliance on empirical, human-centred designs to explore behavioural trends and barriers to digital adoption. For instance, Jin and Fan (2022) provided a qualitative analysis of older adults’ use of physical and digital banking platforms in rapidly developing technological environments. Complementing these approaches, the presence of keywords such as Human Experiment, Major Clinical Study, and Controlled Study suggests that some research adopts rigorous experimental or intervention-based methodologies to evaluate cognitive outcomes, such as memory retention, attention, or executive functioning, that are associated with internet use among older adults.

Demographic terms such as Male, Female, Adult, Aged, and Age suggest a comparative research orientation, focusing on variations in digital literacy and behaviour across age groups and gender lines. According to Wu et al., (2019), the impact of age on financial behaviour and decision making remains a critical area of contemporary research. These demographic insights also have broader implications for technology adoption, particularly in FinTech. Compared to older adults, younger consumers typically exhibit greater interest and willingness to adopt FinTech. Supporting this trend, a study conducted in India regarding the e-banking adoption behaviour confirms that, except for marital status, all other demographic variables such as gender, age, monthly family income, educational qualification and internet usage experience had a significant influence (Chauhan et al., 2016). Further highlighting the demographic divide, a study in Indonesia shows that among the older demographic, the gender gap in digital literacy is noticeable, with men being more digitally literate than women (Long et al., 2023).

Finally, Social Support emerges as a critical enabler, illustrating how external networks—such as family, caregivers, and peer communities—shape the digital inclusion and internet accessibility of the ageing population. According to a study conducted in China found that cognitive ability, family support, activities of daily living, social capital, perceived importance, perceived risk appetite positively affected Internet usage among older adults (Shi et al., 2023). These insights collectively highlight the significance of both individual and environmental factors in shaping digital participation among older adults.

Cluster 3: healthcare financing and economic challenges

The colour blue represents Cluster 3. This cluster centres on the economic and financial aspects of healthcare delivery across various age groups, with particular emphasis on middle-aged and extremely older populations (those aged 80 +). According to a study by Sahoo et al. (2021), to achieve equitable healthcare delivery for the older adults in India, focused health finance policies must acknowledge the social, economic and medical determinants of health service utilization and healthcare costs. This cluster examines the financial burden of healthcare services, economic decision-making in medical treatment, and the sustainability of healthcare systems in ageing societies, as indicated by key terms such as health care delivery, health care cost, and financial management. Addressing the challenges faced by the older demographic, requires policymakers, households, governments, and other stakeholders to design a comprehensive health finance plan and demonstrate a commitment to achieving universal health coverage as part of SDG goal 2030 (Panda & Mohanty, 2022).

Cohort analysis within this cluster indicates a methodological emphasis on longitudinal studies tracking healthcare expenditure, utilisation trends, and financial planning across different age groups. According to a cross-sectional study in Sweden by Fledsberg et al. (2023), health care costs increase with age; however, the relationship between age and spending varies by gender and socio-economic categories. The presence of terms such as Clinical Article and Economics reflects the intersection of healthcare policies, economic constraints, and clinical outcomes, suggesting that studies in this cluster analyse how financial factors influence healthcare access and decision-making, particularly among older adults. A study by Glover et al. (2024) among older black adults found that a higher level of health and financial literacy acts as a driver of improved decision making.

The inclusion of adolescents alongside middle-aged and very older individuals suggests a comparative approach, exploring intergenerational differences in healthcare consumption, financial dependency and economic preparedness. As per Cecconi et al. (2025), medical requirements and health care usage vary across generations, with the silent generation uses healthcare more extensively than younger generations. This cluster underscores the pressing need to address escalating healthcare costs and develop viable financial strategies to support aging populations. It offers rich and valuable insights for policymakers, healthcare professionals, and financial advisers striving to optimise economic efficiency in health service delivery. These insights strongly support the design of inclusive healthcare financing models that complement with global policy frameworks such as Universal Health Coverage and SDG 3 (Good Health and Well-being), thereby ensuring equitable access to care for aging populations. Attaining financial inclusivity by innovation of older adult friendly FinTech products will help to achieve SDG 9 which advocates industry, innovation and infrastructure. At the same time, higher adoption of FinTech for the older adults from all spheres of life and across geographies will ensure achieving SDG 10 promoting reduction in inequalities in accessing resources.

In many developing economies healthcare financing has remained catastrophic and pose a serious concern, which can be addressed by proper digital finance mechanisms. Future studies should prioritise these regions to suggest evidenced-based inclusive health policies and interventions. Moreover, future research would also benefit from interdisciplinary integration, especially the application of behavioural economics to further enhance financial decision-making and gerontechnology to evaluate tech-driven healthcare solutions tailored for older adults.

Cluster 4: psychological and organizational dimensions in elder caregiving: health, motivation, and crisis responses

Cluster 4, represented in yellow, explores the intersection of psychology, caregiving practices, motivation, organizational management and health promotion within the context of the COVID -19 pandemic in the United States. COVID-19 radically altered the already vulnerable caregiving environment in the US; highlighting the critical need for systemic changes. This cluster emphasizes the psychological impacts on caregivers, including heightened stress, burnout, resilience and motivational dynamics, while emphasizing the crucial role of family support in both informal and professional caregiving. These results align with evidence suggesting that care givers experiencing care disruptions exhibited higher levels of anxiety, loneliness and depressive symptoms (Truskinovsky et al., 2022). The pandemic has significantly transformed caregiving practices, intensified emotional and physical burdens and hastened the adoption of telehealth and digital health solutions. Ensuring that older adults have access to appropriate technology can significantly reduce disparities in healthcare utilization and promote more equitable access to healthcare services across various age and income groups (Choi et al., 2022).

The organizational and management aspects are central to exploring policy interventions, institutional support systems, and workforce challenges that influence caregiver well-being and patient outcomes. A study by Norful et al. (2024) found that the well-being of healthcare assistants was strongly predicted by increased organizational support and a positive workplace culture. Moreover, health promotion initiatives aimed at caregivers play a crucial role in strengthening their resilience, mental well-being and overall caregiving efficiency. Findings from a review by Khiewchaum and Chase (2021) suggest that interventions such as psychoeducation, can improve caregiver well-being and health. The findings from this cluster offer valuable insights for policy decisions and strategies aimed at improving caregiving sustainability and economic efficiency within healthcare systems.

Technology should promote social networks in tandem with strong institutional frameworks, that are customised for specific community structure and conducive for older adults.

Cluster 5: digital finance, social isolation, and financial well-being

In the context of digital technology adoption, Cluster 5, symbolised by violet, explores the connection between digital financial inclusion, aging, economic factors, and social well-being. This cluster’s primary focus is on older adults’ interaction with digital financial services and the barriers they encounter. The rise of Digital Technology and Digital Inclusive Finance reflects an emphasis on technological advancements to bridge financial gaps for older individuals, particularly through mobile banking, online payment systems, and digital financial literacy initiatives.

Digital Inclusive Finance fosters an accessible, user-friendly and inclusive financial environment for the older generation by lowering barriers to financial service access, addressing personalized financial needs, enhancing financial literacy and promoting innovation in FinTech products. This, in turn, effectively stimulates their consumption potential (Fan et al., 2024). Income emerges as a key determinant, since financial disparities significantly influence access to and use of FinTech solutions. A study by Wang and Mao (2023) found that by eliminating credit restrictions and increasing family income, digital inclusive finance can mitigate the financial vulnerability of aging families. Affordability concerns, shortage of digital skills and technological scepticism further exacerbate exclusion risks among lower income older adults. Income inequality, particularly in developing countries, is identified as a major cause of the digital divide within the older demographic (Mubarak & Suomi, 2022).

Moreover, Social Isolation introduces a critical socio-psychological dimension; older adults with limited social interactions are less likely to interact with FinTech solutions, thereby heightening financial marginalization and economic vulnerability. Evidence suggests that social interactions can significantly boost technological engagement among the older people (Mei, 2024).

To promote equitable financial participation among older adults, this cluster emphasizes the need for tailored interventions, including community-based financial education, digital literacy programmes, and the development of user-friendly FinTech solutions. These insights are highly valuable for financial institutions, policymakers and technology developers aiming to enhance digital financial inclusivity and bridge digital divide among the older population.

Content analysis

Structured content analysis of highly cited articles using the TCM-ADO framework

Table 4 presents a content analysis of the top 55 publications ranked by citation count, highlighting the most influential studies. To provide an analytical depth, the TCM- ADO framework (Theory–Context–Method; Antecedents–Decisions–Outcomes) has been applied, presenting a structured synthesis of each study’s core theoretical base, research context, methodological design, key variables examined, and major findings.

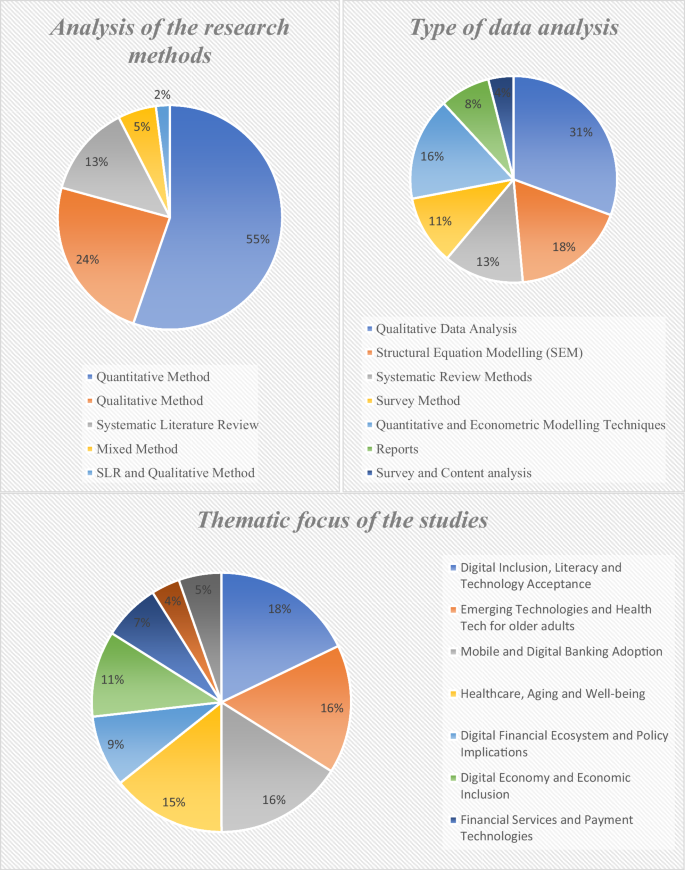

Distribution of research methods, data analysis techniques, and thematic focus among the top fifty cited papers

Analysis of the research methods

An analysis of top 55 articles reveals interesting trends in the research methodologies employed. It is found that 55% (30 studies) employed a quantitative method, 24% (13 studies) adopts a qualitative approach, 13% (7 studies) follows a Systematic Literature Review approach, while 5% (3 studies) of the studies accounted for mixed method approach.

Type of data analysis

The data analysis techniques adopted by the top 55 articles demonstrate a diverse methodological landscape. The most frequently used methods include Qualitative Data Analysis (31%), Structural Equation Modelling (SEM) (18%), Quantitative and Econometric Modelling Techniques (16%), Systematic Review Methods (13%), and Survey Method (11%).

Thematic focus, derivation, and reliability

Themes were derived using a structured content analysis, guided by the TCM–ADO framework. The framework is designed to guide the criticality of the analysis and ensure that the resulting themes are conceptually robust and connected to established scholarly dimensions. The process was primarily inductive, involved a detailed reading and interpretation of the texts in order to establish dominant themes. To enhance the results reliability, two researchers independently classified the studies into themes, and all discrepancies were resolved by achieving a consensus. This approach, integrated within our tri-method design (systematic review, bibliometric analysis, and structured content analysis), strengthens transparency and replicability of the critical observations obtained from the review. Definitions of the category are provided in Appendix C.

Figure 9 illustrates the distribution of research methods, data analysis techniques and thematic focus among the top 55 cited papers, offering insights into the methodological and topical trends in the existing literature. Exploration of the key themes and research topics of the most impactful articles on the FinTech adoption among older adults, highlight nine main research areas categorized into percentage groups. The thematic distribution is as follows: 18% (10 studies) focus on ‘Digital Inclusion, Literacy and Technology Acceptance’, while ‘Emerging Technologies and Health Tech for older adults’ and ‘Mobile and Digital Banking Adoption’ each account for 16% (9 studies) followed by ‘Healthcare, Aging and Well-being’ at 15% (8 studies). Themes related to ‘Digital Economy and Economic Inclusion’ and ‘Digital Financial Ecosystem and Policy Implications’ represent 11% (6 studies) and 9% (5 studies) of the studies considered for the content analysis. Further, Financial Services and Payment Technologies comprise 7% (4 studies), while Risk Management and Safety make up 5% (3 studies), and Cross-Cultural and Transnational Perspectives account for 4% (2 studies).

Distribution of research methods, data analysis techniques, and thematic focus of the top fifty-five cited papers.

link